Trade Review and Lessons

December 3, 2024

6 mins

.jpg)

A lot of our trading decisions boil down to evaluating between probabilities. However the laws of probabilities, which are true in generalisations are often misleading in specifics.

Traders are not paid in probabilities; they are paid in Rupees. Lets dig deeper :

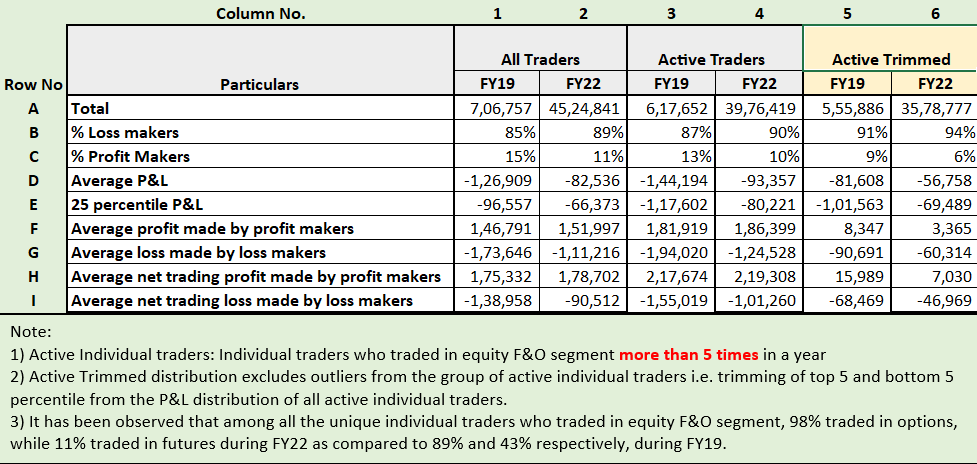

Every day, when we log in to our broker accounts, we are greeted by the SEBI Risk disclosure, which states that 90% of F&O traders incur losses. Even though I don't trade in derivatives, it is still unpleasant to start a trading day by seeing the general probabilities skewed against us. I feel like a smoker who ignores the grotesque image on the box while opening it. I went through the SEBI study (dated January 25, 2023) again and observed some devils in the details -

a) An active trader is defined as someone who has executed more than 5 trades in a year. I believe that the threshold used to classify a trader as "active" is unreasonably low.

b) The sample is heavily skewed towards options with 98% trading options in FY22. It's primarily O rather than F&O.

c) The total number of traders in the sample has increased by 5.4x, from 7.1 Lakh in FY19 to 45.2 Lakh in FY22. Assuming that the sampling methodology was the same, it implies that 38.2 Lakh (84%) traders in the FY22 sample set have less than 3 years of trading experience, possibly 2 years if we assume that most of the sample started trading after COVID.

Based on reading the observations collectively, the inference is that ~84% of option traders incurred losses within their first 3 years (possibly 2 years). This differs from the media headlines that appeared. Trading has asymmetry, the individuals who die do so at a very early stage in the game, while those who survive go on to live for a very long time. The average survival is not corelated with the median survival. Additionally, excluding qualitative aspects of trading from the sample size (experience, skill, capital, trade risk) will result in incorrect conclusions. It's like comparing the three photos below and passing judgment on the latter two, with the first one heavily dominating the sample data.

d) The average P&L of all the traders is lower than the 25th percentile P&L (Row D < Row E). In other words, the losses made by the bottom 25% of the sample are greater than the profits/losses of the other 75%. This further highlights the limitations of relying solely on quantitative data, where traders who are gambling without control on risk of ruin are given the same weightage as the traders taking calculated risks.

e) To address this significant skewness, the analysts trimmed the distribution by excluding the top and bottom 5 percentiles (Column 5,6). As a result, nearly half of the profitable traders were excluded, while only 6% of the loss-making traders were adjusted for. This adjustment has reduced the average profit for profit makers in FY22 from Rs 219,308 to Rs 7,030 before transaction costs, and from Rs 186,399 to Rs 3,365 after transaction costs.

This selectively led to the risk disclosure that “those making net trading profits, incurred between 15% to 50% of such profits as trading costs.” A slow clap to the irony here, when we are imposed with multitude of costs and taxes (Income tax, STT, SD, GST, ETC, DP charges, SEBI charges) and then shown this disclosure based on numbers that have been beaten down enough to fit a narrative. Furthermore, removing outliers in a heavily skewed distribution curve will lead to incorrect results. It's like a surgeon saying, "Our operation has a mortality rate of 1%. So far, we have operated on 99 patients with great success. You are our 100th patient, so you have a 100% probability of dying on the table.”

While I am skeptical of the data supporting the narrative, I wholeheartedly agree with SEBI's message. Trading, particularly with leverage, is a high-risk, high-reward endeavour, and the success ratios will always be skewed, even if we clean and reanalyse the sample data. The filth that was being distributed by fraudulent content creators masquerading as traders had to be urgently curbed, even if it required bending the numbers for greater good. Although I have a passion for the craft, it may often be better for the average person to stick with the less efficient strategy of investing in mutual funds for the long term.

Every endeavour that offers high rewards, whether monetary or non-monetary, will also have a high threshold for success and a skewed distribution. Less than 1% of CA applicants clear the course, less than 10% of scholars complete their PhDs, IIT acceptance rate for undergraduate courses is 0.5%, the UPSC pass percentage is 0.2%, only 30% of mutual funds beat the index, less than 1% of traders beat FD returns in a 3 year period. If we solely focus on the math and probability of success, we will only get crippled into inaction and settle for the lowest common denominator of our lives. The tougher challenges in life are often pursued not only for the sake of success, but also for the pure joy found in the relentless pursuit of mastery and accomplishment. As @JerrySeinfeld says, “Your blessing in life is when you find the torture you’re comfortable with - whether its marriage, kids, work, exercise, eating habits. Find the torture you can tolerate and you will do well”.

Probability is not mere computation of odds on the dice or its more complicated variants; it is the acceptance of the lack of certainty in our knowledge and the development of methods for dealing with our ignorance. (By @nntaleb)

When we begin learning to trade, one of the first things we learn is the relationship between win rate and risk reward (RR). It is preferable to begin with systems or setups that have a higher win rate, even if they are inefficient in terms of RR. That’s because our first need is to ensure that the probability of the unacceptable (i.e., the risk of ruin) is nil. Position sizing combined with high-probability setups ensures this foundational protection. But after the few initial years of getting a grip over basics, our next challenge is to scale up the portfolio and overcome mental barriers of taking bigger calculated risks. Scaling up requires you to take additional risks, at least in absolute numbers, if not in percentage terms. This is where your FAITH in your skills are tested more than your skills themselves.

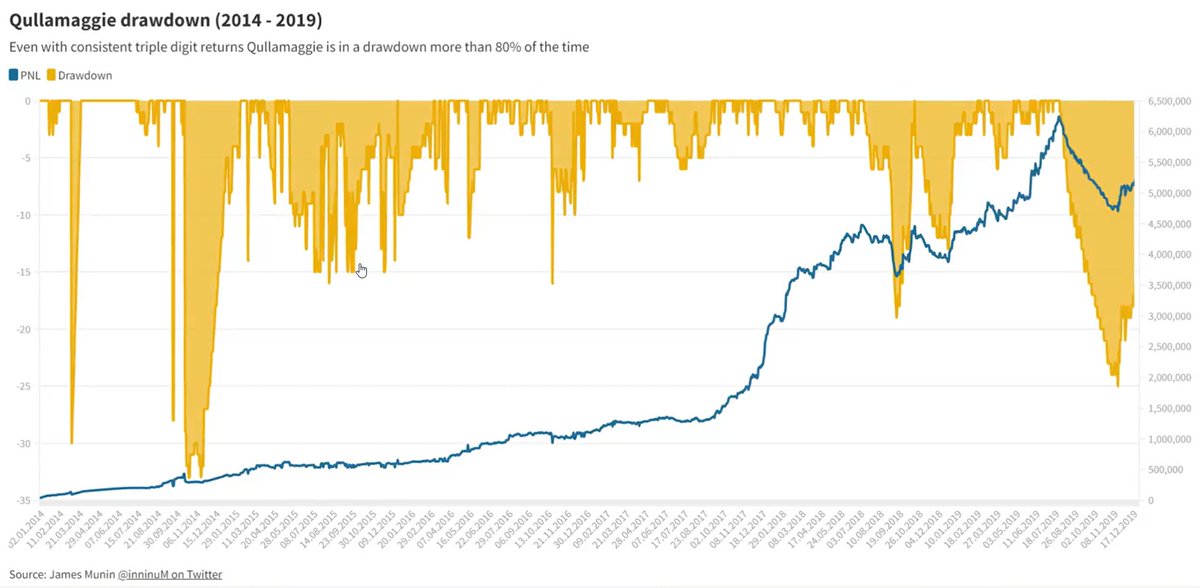

@Qullamaggie and @DanZanger are perhaps two of the most successful individual traders ever, but they regularly experienced drawdowns of 10-30% from their equity curve highs. This graph shows Qullamaggie’s P/L and drawdown curve (by @inninuM) -

If we analyze drawdowns from a unilateral perspective of -25%/+33%, we may inadvertently assume that he is taking risks beyond what is considered normal for other traders.But when you listen to these masters speak, they often repeat things that most of us already know, especially about risk and probabilities. You would often find yourself trading the same setups as them, and you probably use similar trading processes.

However, the intangibles are the biggest differentiator. They have mastered the art of being “uncomfortably” aggressive in positive expectancy (not probability), up to the point where they have FAITH in their skills to recover without the risk of ruin. @markminervini may not have won the 2021 USIC by a wide margin if he didn't have the skills to handle 4x leverage on a stock and its associated volatility, and if he did not have FAITH in himself to recover from its adverse consequences. Higher volatility in the equity curve is often a result of the process of scaling up a portfolio quickly, rather than a flaw.

Every time they put their skills under trial by fire, they strengthened their FAITH in dealing with uncertainty and coming out unharmed. It also developed the mental strength to push harder on the accelerator in favourable markets. The outcomes, which initially appeared low probability on math, gradually transformed into trades with high expectancy because they were willing to venture beyond their comfort zones of borrowed knowledge. Their mental construction directed them to do exactly what other traders avoid doing by generic reasoning of "each to his own" or "depends".

Low probability was not the sole decisive factor for judgment, but it served as an input for developing stronger trade management skills to increase expectancy. Consequences, not probabilities, determine the decisions that matter.

My intention is not to urge you to take excessive risks, volatility or trade in unfavourable markets, but to encourage you to develop FAITH in your skills by repeatedly putting them under trial by fire especially in your formative years, without the risk of ruin. Scaling up your portfolio will require you to overcome mental barriers more than technical ones. Trading psychology mastery is essential for this mental barrier breakthrough. It's not a beginner-level skill, but you also didn't learn to drive just to stay in second gear.

I wrote this more for myself as a reminder to stick to, and perhaps as a spill over for traders who face similar challenges as me.It is easy to start trading but easier to settle for mediocrity once you have started. Developing feedback loops through deliberate trials builds this unshakeable FAITH.

December 3, 2024

6 mins

March 9, 2023

6 mins

July 2, 2023

5 mins